Digital payments in Europe, by country - statistics & facts

Digital payments in Europe vary significantly across the region, often not at all reflecting a "European single market". One can already observe this, for example, in estimates on the share of cash within multiple European countries. The diversity within its payment landscape is perhaps one of Europe's defining features. Nevertheless, what are the main trends when it comes to payments in Europe?

Europe has many digital payment methods, brands, and preferences when it comes to payments. The question of how to unify all these different approaches - even between neighboring countries - will be one that could shape the European payments landscape for years to come.

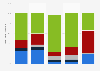

Debit cards, not credit cards

Typically expected to be similar to the United States when it comes to credit cards, the opposite holds true for Europe. Credit card use in Europe was highest for smaller countries that rely on cross-border e-commerce, such as Iceland or Switzerland. Debit card penetration in several European countries, on the other hand, was significantly higher. Still, Europe's diversity can still be observed in the most used payment card brands within European countries: The United Kingdom favored Visa, whereas Sweden used Mastercard the most. France, Denmark, and Italy had their own in-market payment card solution.Local innovations vs. international brands

The differences between Europe's countries also show elsewhere. Europe's main examples of A2A (account-to-account) payments - bank transfer payments, made possible by Europe-wide regulation PSD2 - are in Poland (BLIK) and the Netherlands (iDEAL), not in Europe's largest countries. Those countries, instead, prefer international brands. Germany and Italy, for example, ranked among the most likely countries in the world to use PayPal, with consumer responses close to those from the United States. This difference could potentially be attributed to international schemes first rolling out in Europe's largest economies, foregoing smaller countries. This may also explain why some of the most downloaded BNPL apps in Europe were first developed in Europe's smaller economies.Cross-border payment issues, and how to solve them

The European Union is trying to fight the differences in payment systems between its members. Digital wallets are not a focus here. One of the fastest growing payment methods worldwide, wallets are not popular enough in Europe compared to elsewhere. Instead, the EU is testing A2A payments - specifically, it expands the Netherlands' iDEAL system, which is built around bank account transactions - to help improve cross-border payment speed and reliability. The resulting app, Wero, is available in a handful of countries in Europe. It is unclear whether the digital euro could fulfill such a role as well.Europe has many digital payment methods, brands, and preferences when it comes to payments. The question of how to unify all these different approaches - even between neighboring countries - will be one that could shape the European payments landscape for years to come.